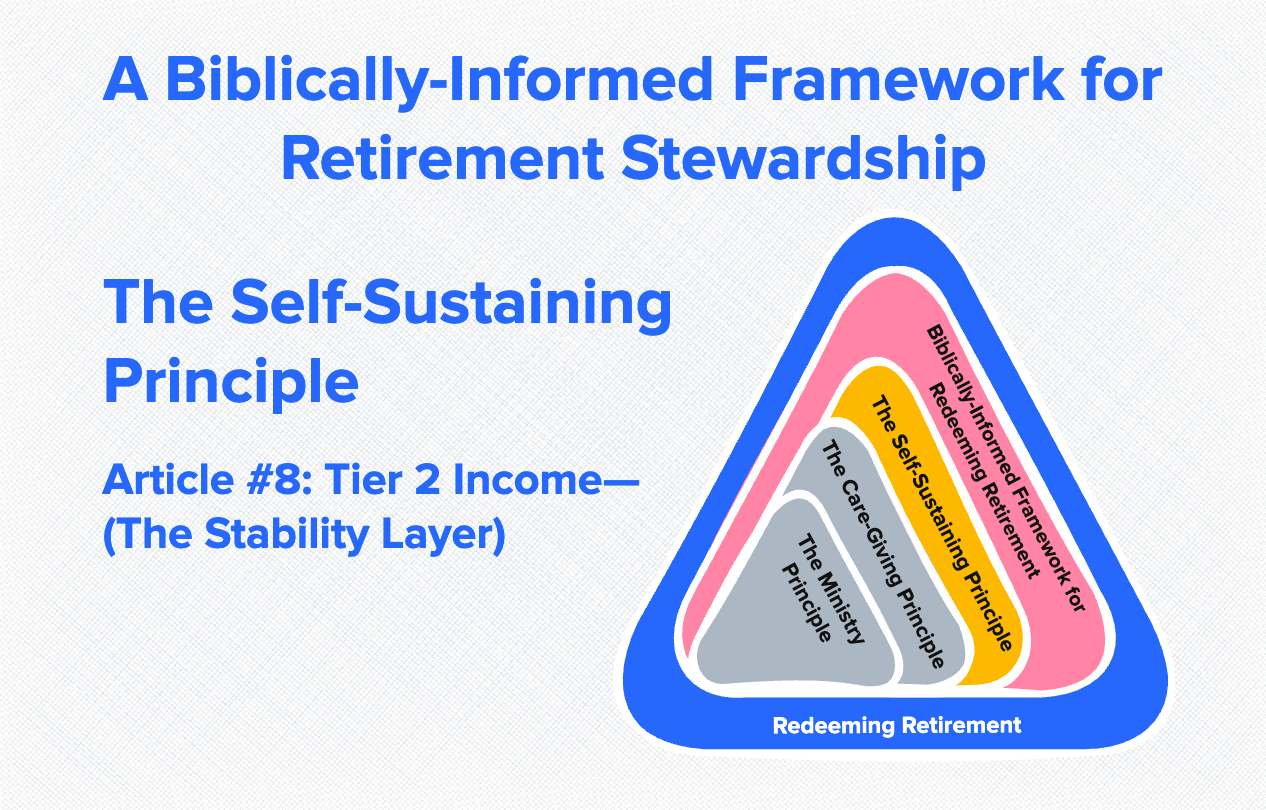

The Self-Sustaining Principle—Article #9: Tier 3 Income (Portfolio Withdrawals and Variable Income Sources)

This article is part of the Biblically-Informed Framework for Retirement Stewardship (BIFRS) series. In this article, we’ll explore Tier 3 income. This variable, self- or advisor-managed layer sits atop your guaranteed income (Tier 1: Social Security, pensions, annuities) and semi-stable income (Tier 2: bonds, dividends, TIPS). It’s the most flexible part of your retirement income, … Read more