TaxesInvesting & Taxes6 Min Read cjcagleonJuly 4, 2025The New “Big Beautiful” Tax Bill As you’ve most likely heard, there is big news coming out of D.C.: The so-called “Big Beautiful Bill” passed just before the… Read More

SpendingSaving for RetirementDave Ramsey12 Min Read cjcagleonMay 27, 2025Financial Gurus vs. Economics Professors Before I had heard of David McKnight and his books or read his most recent, The Guru Gap, I read a paper by Professor James J. Choi from Yale… Read More

Finishing WellFaith & Kingdom Living10 Min Read cjcagleonMay 14, 2025Ever Wonder What They’ll Say About You When You’re Gone? I don’t often write about these kinds of topics. But if you are near or in retirement, as I am, you know you are in the final third or… Read More

Online SecuritySpendingLifestyle & Health11 Min Read cjcagleonApril 29, 2025Understanding PayPal, Venmo, Zelle—and Now Paze (and How I “Invented” It!) A friend’s wife texted me a while back asking about “Paze.” I hadn’t heard of it then, even though, as I’ll explain later, I practically… Read More

Finishing WellFaith & Kingdom Living12 Min Read cjcagleonApril 15, 2025John Piper’s Framework for a Biblically Informed Retirement Plan When most people think about retirement planning, they picture calculators, spreadsheets, and savings goals. But for Christians, retirement is… Read More

TaxesPortfolio7 Min Read cjcagleonApril 8, 2025Trump’s Tariffs: What They Are, What They Aren’t, and Why It Matters to Retirees Trump’s tariffs are very much in the news right now. While the downsides of tariffs often get more attention, rightly so due to their… Read More

SpendingPortfolioInvesting & Taxes9 Min Read cjcagleonMarch 26, 2025What Kind of Returns Do You Actually Need in Retirement? Well, it’s baaaaack…and you know what: stock market volatility. And it came back with a vengeance a few weeks ago, moderating some in recent… Read More

TaxesInvesting & TaxesSocial SecurityLifestyle & Health9 Min Read cjcagleonMarch 11, 202525 Things Retirees Tend To Worry About (But May Not Need To) The Dictionary of Bible Themes defines worry as “A sense of uneasiness and anxiety about the future. Scripture indicates that such anxiety is… Read More

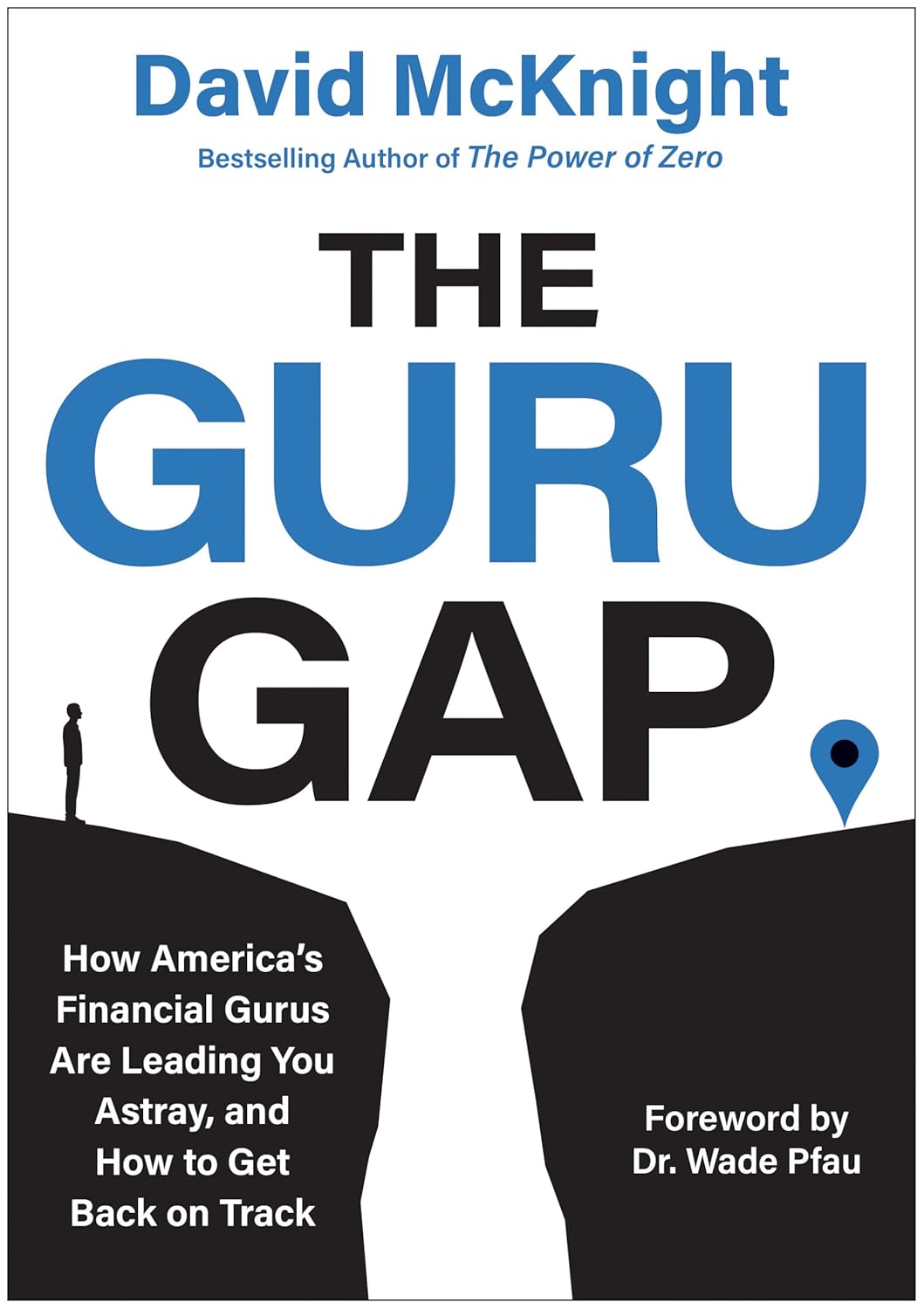

AnnuitiesInvesting & TaxesDave Ramsey8 Min Read cjcagleonFebruary 25, 2025My Thoughts on “The Guru Gap” Generally speaking, there are two “camps” (or schools of thought) for investing for and creating an income stream in retirement.… Read More