Sooner or later, most of us will ask ourselves this question: “Can I retire?” Perhaps because of an unexpected layoff, a health issue, age, or some other factor, we will need to come up with an answer.

No matter what the reason or when you decide to retire, you will need to have some idea of how you are going to fund your retirement, especially if your plans include little or no work for pay.

Planning is proper and part of wise stewardship (Luke 14:28), as long as we commit our plans to God (Prov.16:3), and hold to them loosely realizing that he alone determines their outcome (Prov.16:9).

In fact, financial planning for retirement is one of the major life “slices” that I identified as part of the Retirement Stewardship “Wheel of Life.” It is one of the most important because you have to have some kind of financial plan in place to be able to retire with dignity.

Before I go further, I want to restate and reemphasize my usual disclaimer that the things I cover in these next three articles may well require you to seek professional financial advice that is specific to your situation. There are more variables involved than I can cover here, so if you are hesitant to do this for yourself, then, by all means, enlist the aid of a qualified financial professional. The information I will provide in these next three articles are concepts and a high-level process that you can use if you are so inclined.

The big picture

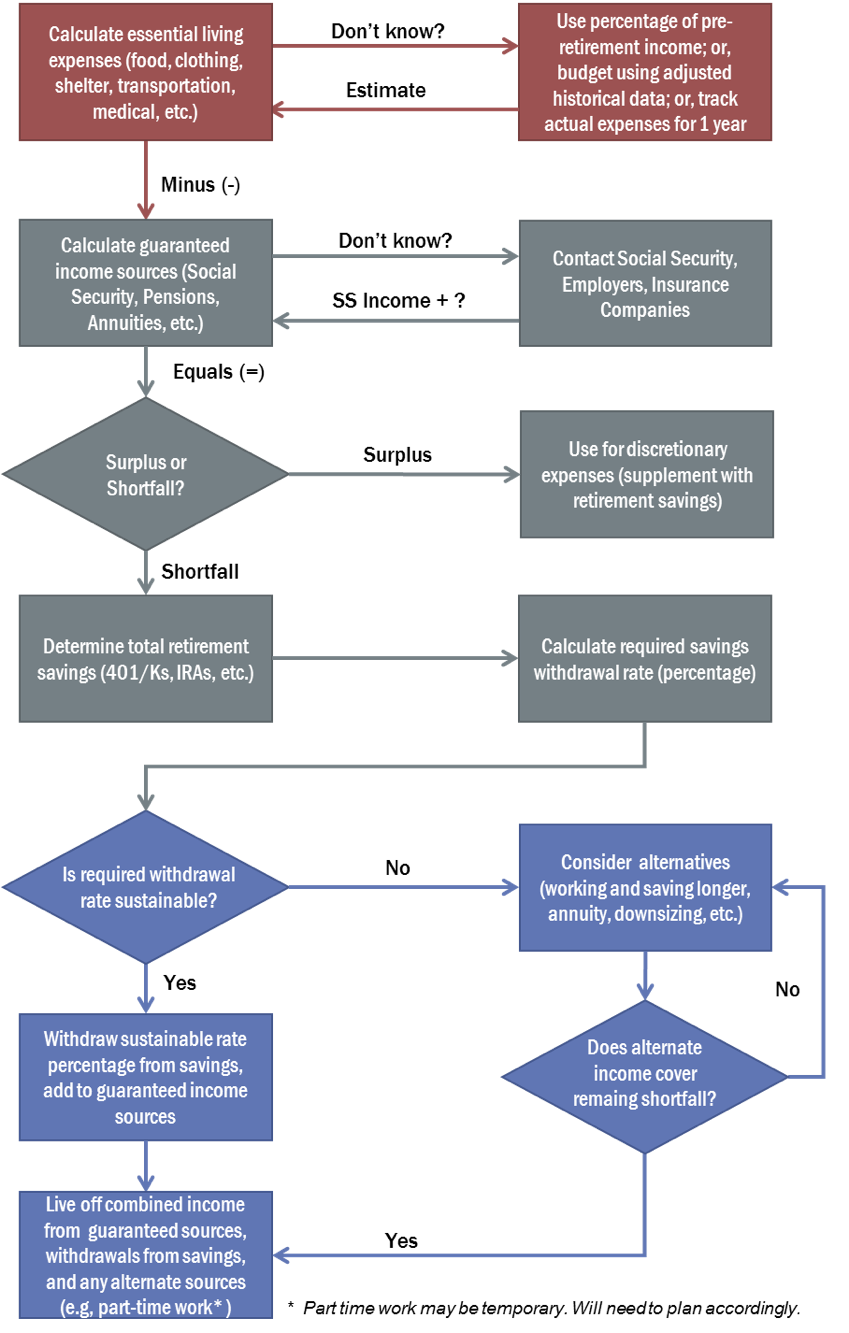

There are a lot of moving parts (variables) that factor into the retirement financial planning process. To help you visualize it more holistically, I have created a process flow diagram that describes the big picture and highlights the different planning phases via color-coding. It may look a little scary, but please bear with me – it’s easier than you think, it just takes some time and effort, and a little math.

As you can see, the diagram is structured around three parts, each of which is color-coded:

- Determine your essential living expenses (in red)

- Identify and quantify your income sources (in gray)

- Decide whether you are financially able to retire (in blue)

I plan to do an article on each phase, starting with the first one: identifying your expenses.

Know your expenses

If you are getting close to retirement and I was to ask you how much you need to have saved you may have a hard time coming up with a precise figure. Will you need $100 thousand? $300 thousand? $700 thousand? $1 million or more?

Sure, it would be good to have a savings target, but based on what? For many, it’s the number that will ensure that they will never run out of money. But given all of the unknowns of living 20 or 30 years in retirement, how can we possibly know what that number should be? Perhaps there are other numbers that we need to think about before we can determine if our savings goals are on-target.

What if I asked you how much income you need per month to meet your expenses? You could probably come up with a more accurate number because that is how you managed things your entire life. Like most, you just tried to match income to expenses (and hopefully the former was a little higher than the latter).

I think the number that you need to begin with is your estimated expenses in retirement – what you think your bills will be after your paychecks stop. Having that number in hand is the first big step of the planning process.

As shown in this part of the diagram, at a minimum, you need to cover your essential living expenses (food, clothing, shelter, transportation, taxes, medical expenses, etc.). Many of you will also include giving as part of your regular essential expenses.

To start with, we’re just talking about meeting your essential needs – those that are non-discretionary. That will provide you with the lowest possible expense baseline that you need to be able to fund in retirement.

And remember, although you need “shelter,” you don’t necessarily need a five thousand square foot house with a large mortgage. When you calculate your expenses you’ll have to decide whether to include the large house and mortgage or something more reasonable in proportion to the amount of income you will have to cover them. You could start with the larger housing expense and then adjust as conditions warrant.

If you have already been tracking your expenses, this should be pretty easy. But you will still need to make adjustments for living in retirement. Some costs will stay the same; for example, your utility bills if you remain in your pre-retirement home. Others may change due to a change in location or lifestyle.

There will probably be some things that will change just because you are retired. Many of the expenses directly associated with your employment will go down, although the loss of certain employee benefits such as low-cost group medical insurance could offset them. Here are some of the major categories to consider:

Social Security taxes

Your Social Security taxes will go to zero when you stop receiving a paycheck. The amount of that reduction will be equal to or less than 6.2%. If your salary exceeds the Social Security cap ($128,400 per year in 2018), then you only pay the tax up to that amount. However, if you are self-employed, you are also paying the employer’s portion, which is another 6.2%.

So, if you are an employee and your total income in 2018 is $75,000, you would pay $4,650 in Social Security taxes. If you’re self-employed, you’re paying twice as much, which is $9,300. That’s a 12.4% expense reduction right from the start.

Of course, don’t forget your spouse — he or she may be paying these taxes too.

Medicare taxes

Like Social Security, your Medicare tax will also go to zero when you retire, a reduction of 1.45% of your total salary. Unlike Social Security, there is no cap on the income that is taxed for Medicare. This rate applies to the income from both spouses, and like Social Security, self-employed people must pay the employer’s rate too (another 1.45%).

When you retire, you will probably start receiving Medicare benefits. You won’t pay the taxes anymore, but you will pay premiums (for Part B and any supplemental plans). They will take the place of whatever you were paying for your employer-sponsored or individual health care plan. In my case, that will mostly be a wash.

Contributions to retirement accounts

In general, your contributions to retirement accounts will go to zero when you retire. For example, if you’re contributing 6% of your income to an employer’s 401(k), your expenditure rate will decline by that amount when you retire. If you’re making $75,000/year, that’s another $4,500/year that won’t be coming out of your paycheck. But as a consequence, you won’t be contributing to your savings or getting your employer’s match anymore either – you’ll probably be withdrawing from it instead.

Some people contribute to both an employer-sponsored retirement account (401/k or 403/b) as well as an Individual Retirement Account (IRA). They may even add to other taxable accounts. It’s probably a fair assumption that you’ll also halt contributions to such accounts when you retire, at least to the retirement accounts. I used to contribute to both a 401/k and an IRA, but now I only add to a 401/k so I can get the employer match. Once I retire, I will stop altogether – you probably will too.

You may also decide to move money from a taxable, non-retirement account to an IRA so that it can grow tax-free after you retire. But that isn’t an expense from income – it’s a transfer of money from one kind of account to another. (I’m not talking about an “IRA Conversion” – that’s a different subject altogether.)

Union fees and professional costs

These are probably relatively minor for most people, but you may not have to continue to pay certain unreimbursed membership fees, registration fees, travel costs, etc., associated with your employment.

Commuting costs

These include things like gasoline, auto repairs, car insurance, highway tolls, and possibly mass transit fares. These costs can be somewhat substantial for commuters who drive long distances.

In the metropolitan area where I live (Charlotte, NC), many people drive 10 to 15 miles to work each day, some longer. After you retire, you won’t need to commute to work anymore, so your gas costs could go down. Other costs, such as insurance and maintenance, may also be less.

Disability and life insurance

You may be paying for disability and life insurance through your employer. Those will probably cease when you retire unless you carry them forward as private insurance policies. If you have them outside of your employer, you may not need them any longer, especially if you are “self-insured.” I have a term life policy through my employer and also one privately. I plan to terminate both of them once I stop working.

Children and education expenses

These have little to do with whether you are retired or not. You may be helping out adult children or older children (or grandchildren) with education or other expenses. That has to be considered a discretionary item in retirement. So if you are paying them before you retire, you may have to stop after you retire, depending on your income.

Personal expenses

Once you stop working full-time, other expenses such as clothing and other personal items, eating out, etc. may be less. That is especially true if your work requires you to maintain a particular type of wardrobe or to pay certain out of pocket expenses.

Each situation is different

Of all the expenses listed above, the largest reductions will probably be your “Social Security and Medicare Taxes” and your “Contribution to Retirement Funds.” They could total anywhere from 15 to 25 percent or more depending on your income and savings rate. They would NOT include any contributions made by your employer (e.g., 401/k or 403/b matching funds), but it does include the contributions to tax-deferred accounts as well as taxable ones, should you stop contributing to them.

When you factor in other reductions and include only your essential living expenses, you may find that the number is lower than you expected.

But there are a lot of things that can push that number higher. Many retirees end up spending more in retirement than they did before. But that’s usually due to higher discretionary expenses for recreation and travel.

Each family’s situation will be different. Your essential living expenses as you enter retirement will be largely determined by your expenses before you retire and your lifestyle choices afterward.

What if you don’t know?

If you aren’t managing and tracking your expenses at some level of detail before you retire, you may have a harder time coming up with an estimate. But do try to come up with one; otherwise, the rest of the financial plan becomes rather pointless.

As I noted in the box on the right side of the diagram for what to do if you “don’t know,” here are some suggested approaches:

Use a percentage of your pre-retirement income

A relatively simple method you will often hear is to use a percentage of your pre-retirement income (usually between 60% and 100%). If you are making $75,000 a year and think you can live on 80% of that, then you will need at least $60,000.

The problem is that it’s just a guess. How certain are you that your essential expenses will be $60,000? If you are currently spending exactly what you make, it would be helpful to know how much of that is going toward essential expenses and how much is discretionary. If your discretionary spending is $20,000/year then your essential expenses before retirement are $55,000, not $60,000. If you can reduce your essential expenses by 20%, then you only need $44,000, not $60,000 based on the 80% estimate.

The difference between $60,000 and $44,000 is not insignificant. Based on a 4% annual withdrawal rate, it takes $400,000 in savings to fund the difference of $14,000/year in income!

Use average spending data

Another way to approach this is to use averages. As a starting point, we’ll consider the living expenses of an average couple in their mid-60s with no children at home. According to figures compiled by the Bureau of Labor Statistics, such a couple’s spending will come in around $48,000/year.

According to the Census Bureau, the median income in the U.S. for 2016 was $57,617. So 50% of the population is getting by on less than that. If you want to use an average or median number to come up with an estimate of essential living expenses, you may need to adjust it up or down based on your situation.

Prepare a retirement expense budget

For those who want more a more accurate estimate, you could sit down with a basic set of essential expense categories and go through your various financial account statements to try to estimate a monthly or annual amount for each category.

If you do that, consider the categories that are most likely to change after you quit working, which I listed above.

Track your expenses for a year

Perhaps the best way to deal with the uncertainty is to track all of your costs, in detail, while living a “retirement lifestyle.” You could do that for a year before you retire. It may be challenging for some people, but if you want accurate numbers, that is the best way. Alternately, you could take your chances and do it during your first year in retirement and then make the necessary adjustments going forward.

Plan for your unpredictable expenses

Every family has its lifestyle, and unless you make really big changes, such as a significant downsizing or moving from a very high cost of living area to a lower one, your cost of living is not likely to change dramatically on the day of retirement.

I don’t expect to experience any dramatic changes the day I retire. My goal is to start out with my modified retirement budget, which is mostly based on our current expenditure levels with a few adjustments, and then just see how various line items change during the first year and make the necessary tweaks.

Even if you’re successful in coming up with a retirement budget, there is some “expense risk” beyond just the essentials due to unpredictable expenses. Most living expenses are relatively predictable, but some are random.

You can predict with a high degree of certainty that you will have a grocery bill, an electric bill and an internet bill next month, and you can probably predict the amounts fairly accurately. So, if your essential expenses are $45,000/year, you can be pretty sure about that.

But you could also have a major unpredictable expense, so your actual living expenses could be higher – much higher – than $45,000 in any given year. Of course, you could also make discretionary spending choices that increase that number as well.

When your car breaks down, or the water heater fails, or you have to go to the urgent care center for an injury, you have to deal with unplanned and unpredictable expenses. Living expenses can have both unplanned and unpredictable aspects, and that means that your total annual essential expenses are, at least to some extent, unpredictable.

The best way to deal with these unpredictable expenses is to establish a “contingencies” fund and to assume that you will need to replenish it from time to time and include that in your “essentials” budget. If you don’t, you will end up having to take it from other savings, or worse, put it on a credit card.

Next steps

Once you have a pretty accurate accounting of your essential living expenses, you’re ready to go to the next step: Identifying and quantifying all your income sources. We’ll tackle that in the next article: Can You Retire? Part 2: Your Income.