I know quite a few people who have taken an early “traditional” retirement. By that I mean they were between age 62 and 66 and relying on Social Security, retirement savings, possibly some part-time work, and perhaps a pension to supply the income they need in retirement. A relatively common thing among them is their decision to start receiving Social Security (SS) retirement benefits early, at age 62.

Other than the decision about when to retire, when to start taking SS retirement benefits, which come in the form of a lifetime inflation-protected annuity, is one of the most important decisions a retiree makes. Because you can start collecting 75 percent of your “full retirement age” (FRA) benefits at age 62, many choose to do so to help with an “early” retirement. (The average retirement age in the U.S. is 63, three years less than the current FRA of 66.) But each year you wait, your benefit increases until it reaches full benefits level at age 66. The thing is, full benefits are not the same as maximum benefits. Your full benefit can keep growing after age 66 at 4 percent per year, or 32 percent more in total, if you wait until age 70.

Almost everything I have read and studied on this subject suggests that most retirees should not start collecting benefits at age 62. But approximately 60 percent of eligible retirees do. I know that sometimes it is out of necessity, but this divergence between expert opinion and common practice is surprising but in line with the average ‘early’ retirement age of 63.

I have looked at the numbers previously (my wife and I will reach our FRAs next year), and I am generally in full agreement with the experts – collecting early is not the best decision in the vast majority of cases. But because everyone’s situation is different, that is not true in every case. There is some simple analysis you can do to see what makes the most sense for you.

Simple break-even analysis

The main data point that is typically used to analyze the potential advantage of delaying benefits is what is called the “break-even point.” The break-even point is the age at which your cumulative income is the same when two different alternatives are being considered. The conventional wisdom is this: If you think you will live longer than that age, then better to wait to receive your benefits. If you will live less than that age, then better to start earlier.

The main challenge, of course, is that only God knows how long we are going to live (Psalm 139:16). We may have some idea based on current health, family history, the individual choices we have made, etc., but in the end, God determines how many years we will have on this earth. So, the best we can do is to make an educated guess and plan accordingly.

To illustrate, let’s look at a simple example. Say your FRA benefit (at age 66) will be $10,000/yr. If you take benefits early (at age 62) you will receive 75% of your FRA benefit, or $7,500/yr. If you wait until age 70, your benefit will be 132% of your FRA benefit or $13,200/yr. Right away we see a big difference between taking benefits at age 70 versus age 62 (approx. $5,700/yr. higher, for the rest of your life). For some, that could be the difference between being able to pay their bills or not in later life. A simple tabular representation would look like this:

| Full retirement age | 66 |

| Monthly benefit at age 62 | $625 |

| Monthly benefit at age 66 | $833 |

| Monthly benefit at age 70 | $1,100 |

The results of a breakeven analysis of our example show that delaying until age 70 takes approx. 11 years, or until age 80, to break even with benefits starting at age 62, and it would take 13 years, until age 83, to break-even with benefits starting at age 66. If you start benefits at FRA (age 66), it will take 12 years, or until age 77, to break even with benefits at age 62.

That is a lot of good information, but how should you interpret it? More importantly, how does it apply to your situation?

Well, first of all, if you are married the numbers would be different. That’s because, under current SS rules, a non-working spouse without enough “credits” to receive benefits on their own is entitled to 50 percent of their spouse’s benefits. (Earlier “file and suspend” provisions that enabled the primary SS beneficiary to delay their benefits so that they could continue to grow while at the same time receiving the spousal benefit were ended by the Congress in 2016.)

Applying the spousal benefit to our example changes things somewhat. Delaying until age 70 pushes the break-even point out to age 82 versus starting at age 62, and to age 88 versus starting at age 66. If you start at age 66 instead of age 62, you’ll break-even at age 78. My simple analysis is that the best case scenario for couples at this level of benefits is waiting until at least age 66 if they think at least one of them will live beyond age 78, which is a pretty good probability, actuarily speaking. Waiting until age 70 provides only a marginal additional benefit because the spousal benefit doesn’t increase after age 66.

According to the Society of Actuaries, there is a 48 percent probability for couples where both spouses are healthy and make it to age 65 that one of them will live to age 90. So, let’s be conservative and assume that you or your spouse will live to age 90. If you started receiving benefits at age 66 instead of 62, that is 12 years of benefits beyond age 78, which was the break-even point. The total benefit from age 78 to age 90, assuming only one spouse, would be $120,000 ($10,000 x 12 years).

As you can see, the best scenario in terms of cumulative benefits for someone who believes they or a spouse will live to at least age 90 is to defer receiving benefits until age 70. If you knew for certain that you’d live to age 90 or beyond, it would be a no-brainer. Unfortunately, as I noted above, we can’t know that for sure.

That said, this would be my reasoning: Better to believe that you will live to age 90 and get the larger payout during a time when you may need it the most (due to the higher risk of running out of your savings as you age) than to assume that you won’t and take a lesser amount during a time when you may be better able to supplement it with your savings. The latter would deplete your savings faster, thereby possibly cause you to run of savings sooner than expected.

But to be fair, I need to point out that breakeven analysis alone is not sufficient to tell you what you should do. You may decide to intentionally “front-end load” your retirement income with early SS benefits in return for a reduced benefit later on. Many want that income when they can be most active, realizing that they may have less need for it later in life. Others just don’t think they’ll live to age 90; in fact, some will not make it to their average life expectancy of 80 or 85. (As I stated above, only God knows.) If that happens to you, and you waited until age 66 to age 70, you will lose money in the long run. You need to factor all of these things into your decision.

Another analysis approach

Another way to think about SS is as the purchase of an inflation-protected bond from the government that produces income that you defer for some number of years. But it has some unique features: It pays a coupon ( payment on a bond as a periodic interest payment that the bondholder receives) for as long as you live but does not return principal at termination. SS is basically like an inflation-indexed lifetime annuity, as I mentioned above. If you die younger than expected, you lose – sorry, that’s just the way annuities work. But the longer you live, the higher the effective yield. Thinking of SS this way makes sense because it helps you compare it with other financial assets that you may have and as part of your larger financial picture in retirement.

An article on Nerds Eye View, the website of financial planning expert Michael Kitces says,

…the decision to delay Social Security can be evaluated based on the implicit rate of return it creates by choosing to delay, and over longer time horizons – when [you] may “need the money most” as [you] have more years of retirement expenses to cover in the first place – the return of the Social Security delay becomes quite compelling. In fact, the return is generally far superior to any risk-adjusted returns that can be achieved over comparable time periods by the available alternatives, whether investing in risk-free bonds, growth equities, or buying a commercially available annuity. And because the system is indexed to inflation, its real returns will be maintained even if inflation rises, and will only become better if longevity continues to increase as well.

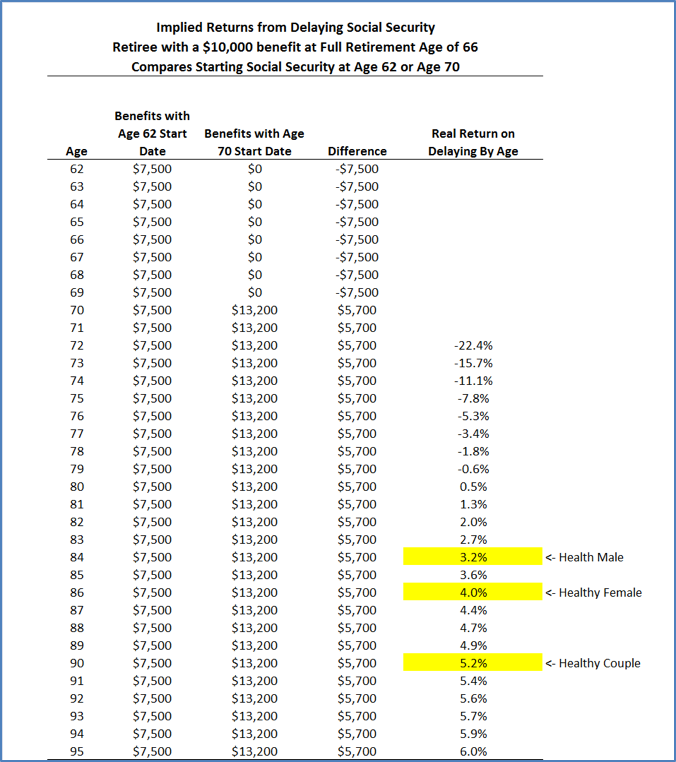

Writing in Forbes magazine, another independent industry expert, Dr. Wayne Pfau, created a table that shows the various rates of return for a retired individual at age 62 with a FRA of 66. (I used the same numbers in the break-even analysis above.) In this example, if you wait until age 66 to start taking benefits, you will receive $10,000 a year. Pfau notes that the $10,000 is an inflation-adjusted number shown in current dollars; therefore, the actual number will be higher.

Just like the break-even analysis, if you start receiving benefits early, at age 62, you will receive $7,500/yr., but if you delay until age 70, you will receive $13,200 in today’s dollars for the rest of your life.

According to the SS Administration, as of 2016, a typical 62-year-old man can expect to live to about 84. A woman can expect to live to 86. If you are healthy, educated, and fairly well-off, you can tack on a few more years (but remember the “God is sovereign” clause). (Remember, there is also a 50/50 chance that at least one will live to be 90!)

As you can see from the chart above, if you start taking benefits at age 62, and then die early at age 75, your real return will be a minus (negative) 7.8 percent – not good. That’s because you have not lived long enough to make up the difference between what you have already collected and the additional income you would have received if you had waited. If you die at age 79, you have essentially reached the “break-even point” where your return is approximately zero percent. By that time, you have collected for enough years to make up the difference. But if you live a little longer than average to the ripe old age of 88, your expected yield rises to 4.7 percent, tax-free. As Kitces pointed out, that is much better than any other “safe” investment that is currently available.

Because some may think that they can claim early and then take their chances in the stock market to make up for the lower payments in the future, Pfau says, “you would take on a great deal of market risk and could end up worse.” I am inclined to agree with him.

Our situation and decision

My wife and I are both turning 65 this year but my FRA is 66. I do not have a pension, but I do have some retirement savings to supplement my SS payments. What should I do?

Previously, when the “file and suspend” provision was in place, it was a pretty much a no-brainer for us. I was going to file at my FRA so that we could start collecting my wife’s benefits, and then suspend my benefits until age 70 so that they could continue to grow 8 percent a year. (Where can you get that kind of guaranteed return?) However, as I mentioned above, “file and suspend” was viewed as a kind of loophole and was recently rescinded, so it may make more sense for me to start receiving benefits when I turn 66 so that we can start getting the spousal benefits as well. To see if it does, I needed to do a simple break-even analysis.

The results of my analysis show that our break-even point is at about age 80 for taking benefits at age 66 versus age 70. However, if either of us lives well beyond age 80, starting at age 70 looks more and more attractive. I probably need to think a little more about this and do a bit more analysis, but my conclusion is that I will probably start receiving benefits when I am age 66 if I am retired from my full-time job at that time.

What about you?

Based on the data, unless you are fairly sure that neither you nor your spouse is going to make it past age 79, it’s a no-brainer to delay benefits to at least age 66 and perhaps to age 70 unless you have other extenuating circumstances such as a chronic health issue. Even though the table doesn’t account for it, if you don’t want to wait that long, it makes sense to delay for at least a few years, at least to your FRA.

One of the best things about SS for those who don’t have a lot of retirement savings is that it is a source of income that can reduce the pressure on what retirement savings to cover your living expenses in retirement. If you delay and thereby receive higher SS payments, you can cheaply and easily hedge “longevity” risk, the risk that you will outlive your money. Maximizing benefits is of particular importance to a retiree whose majority of income comes from SS and has no other guaranteed income sources. (An immediate fixed income annuity may also help in that situation.) SS also functions as a simple inflation hedge. Finally, delaying makes your retirement portfolio much more robust relative to a wide variety of risks, including fraud, error, and cognitive decline (similar to an annuity decision).

So, in summary, there are several issues should be considered when making this critical decision:

- Think about your benefits as something other than just a “monthly check from the government.” If you factor them into your overall retirement plans as an “inflation-adjusted lifetime annuity” that you can elect to defer payments from, and that offers after-inflation, risk-free income for life, you can better understand how to compare it to other investments.

- If you have sufficient retirement income (from savings, pensions, annuities, etc.), and both you and your spouse are in reasonably good health and have a history of longevity in your families, you may want to delay receiving benefits until at least your “full retirement age”, or even beyond, in order to maximize your lifetime benefit. As you select a higher age (up to age 70), your monthly benefits will be increased.

- If you begin benefits before your full retirement age, for example at age 62, earned income after starting benefits may reduce your benefits until you reach full retirement age. Previously, this was a long-term impact, but currently, it only applies until you reach your full retirement age.

- Your personal situation may suggest that your retirement years will be limited, things like your current health condition or family history. Such situations are exceptions to the things above and may present a strong case for taking retirement benefits earlier rather than later to maximize the total lifetime benefit received.

Finally, remember that these are important decisions to make, but your future is ultimately in God’s hands. If you have saved relatively little for retirement, then delaying SS benefits could be a big help down the road. So, do what you can to make wise choices, and then put your faith and trust in God.